Revisiting Market Sentiment: From Complacency to Bearishness

“What goes up must come down

Spinnin’ wheel got to go ’round

Talkin’ ’bout your troubles, it’s a cryin’ sin

Ride a painted pony, let the spinnin’ wheel spin…”

(From “Spinning Wheel” by Blood, Sweat & Tears, 1969)

By Scott Welch, CIMA®, Chief Investment Officer & Partner

Reviewed by Carter Mecham, CMA®, IACCP®

We last visited market and investor sentiment back in December 2024. Much has changed since then – we appear to have entered a new market regime – so it seems appropriate to revisit the topic.

As you may remember, back in December we believed that investors and the overall market were far too “complacent” with respect to underlying conditions, and we anticipated a period of increased volatility and uncertainty as we moved through 2025.

So far, anyway, that seems to have been a correct call, but where might we go from here?

Below, we recap what is driving the uncertainty that is driving volatility, examine the health of the economy, and explore why, despite relatively positive conditions, market sentiment has turned decidedly sour.

Regulations, Taxes, Tariffs – and Interest Rates

As a quick reminder, while market fundamentals (valuations, earnings, quality,

dividends, etc.) are supposed to drive longer-term performance, in the short run prices are heavily influenced by momentum and investor sentiment.

While President Trump campaigned on a variety of issues, the three that had the biggest potential impact on the economy and the markets were regulations, taxes, and tariffs.

It is too early to tell if the Administration will be successful in lowering the regulatory and tax burdens facing companies and individual investors, as those will require legislative action, but we certainly have some early results on his tariff policies – and they have not been positive.

It is not necessarily the tariffs themselves since the full force of any changes has yet to be implemented. But the uncertainty surrounding those policies – which Trump has not helped by changing his mind seemingly every other day – has resulted in corresponding uncertainty (fear) by corporations and investors, and increased volatility in the markets.

One thing that has historically been true is that what the market hates most is uncertainty. And we are watching that play out in real time right now.

We are on the record (loudly and often) saying we don’t like tariffs as economic policy. They have rarely if ever been successful other than as a threatened “sledgehammer” approach to gain concessions from trading partners.

Perhaps Trump’s agenda and rhetoric will, in fact, turn out to be simply a negotiating tactic, but the market cannot just take a “wait and see” approach. Companies need to plan now for future investment and growth objectives.

As anticipated, the Fed did not cut rates in its recent March FOMC meeting, but the market is increasingly pricing in a 25-basis point cut at the upcoming June meeting. The economy, inflation, and labor markets, while maintaining surprising levels of resilience, are beginning to show enough signs of cooling to support a June rate cut – though the data we receive between now and then will ultimately drive the Fed’s decision.

We believe the market will respond somewhat positively to a rate cut, but that is already being priced in. On the other hand, we believe the market will react extremely negatively if the Fed does not cut rates in June. It is a highly asymmetrical risk/reward profile right now.

Current Economic Conditions

Let’s begin our analysis by examining current economic, labor, and inflation conditions.

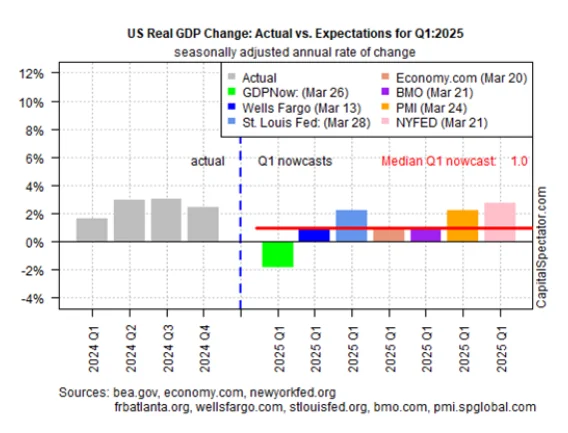

GDP Growth

The collective median forecast for Q1 GDP growth is an anemic 1.0% – not recessionary but certainly not robust.

Source: The Capital Spectator as of March 28, 2025. This is an estimate and subject to change.

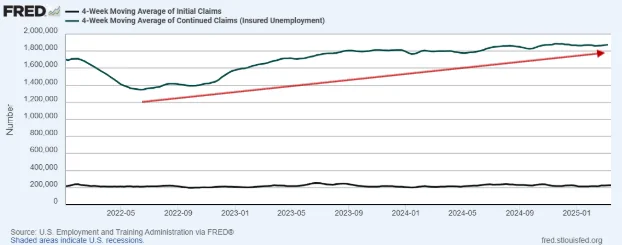

Labor Market

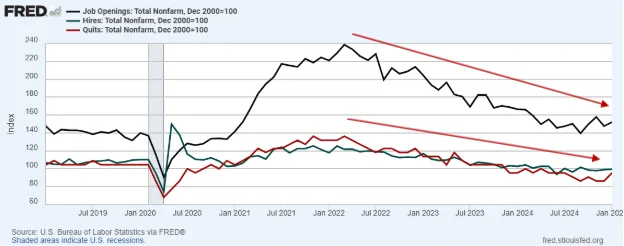

A quick look at the labor markets shows a similar state of affairs – while the labor market has proven remarkably resilient, we are seeing signs of potential cooling.

Source: St. Louis Fed (FRED), data through February 2025.

Source: St. Louis Fed (FRED), data through March 2025.

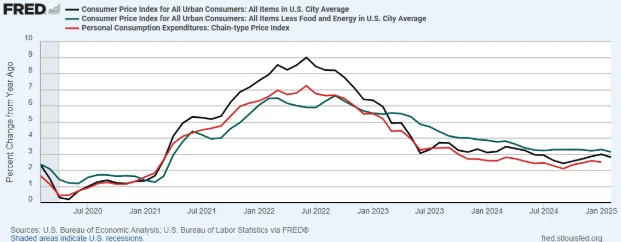

Inflation

Finally, from a macro perspective let’s look at some inflation metrics. We see that inflation remains above the Fed’s targeted 2% annualized rate, it remains somewhat “sticky”, and there are inflationary fears in the market due to uncertainty over the outcome and impact of Trump’s tariff policies. This may make it more challenging for the Fed to initiate a more aggressive rate cut regime.

It’s an interesting dichotomy – Trump is publicly calling for lower rates, but his tariff policies are potentially pushing inflation in the wrong direction!

Source: St. Louis Fed (FRED), 5-year data through February 2025.

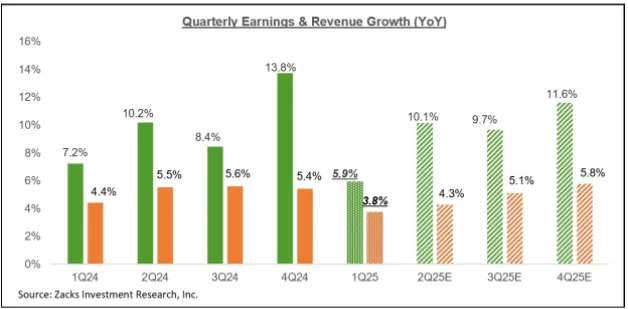

Earnings

Although not technically within the Fed’s mandate, it does pay attention to the stock market (as does Trump), so let’s take a quick look at earnings and valuations in the US.

Large cap earnings and revenues (as measured by the S&P 500 index) posted a solid Q4 2024 earnings season. Expectations are for a decline in growth (though still positive) in Q1, followed by steadily increasing earnings as we move through the remainder of 2025.

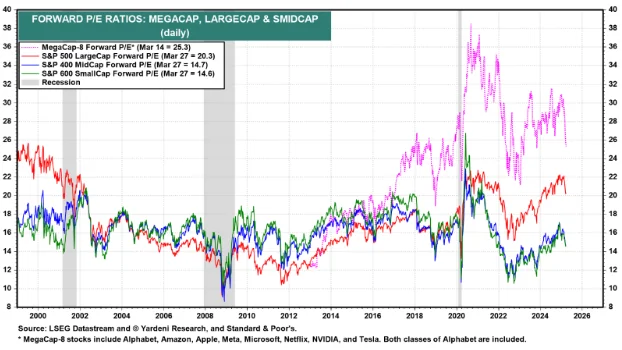

Valuations

From a valuation perspective, despite the recent downturn, the mega-cap tech stocks remain historically expensive (and therefore so do large- cap stocks more generally, since the S&P 500 index is so heavily weighted to those mega-cap stocks). However, small- and mid-cap stocks are currently valued in line with their historical averages.

Source: Yardeni Research, as of March 27, 2025. You cannot invest in an index and past performance is no guarantee of future results.

So, to summarize, the economic, labor, and inflation markets are showing signs of a cooling economy but not necessarily an imminent recession.

Likewise, earnings look to be solid, and valuations are elevated but have fallen below their preceding “frothy” levels.

If these, collectively, were the only metrics that mattered, then one might conclude that consumers and investors should be relatively happy.

But, as we will now see, that is not the case. On the contrary, consumer and investor sentiment has turned decidedly sour.

Market Sentiment: A Bearish Outlook

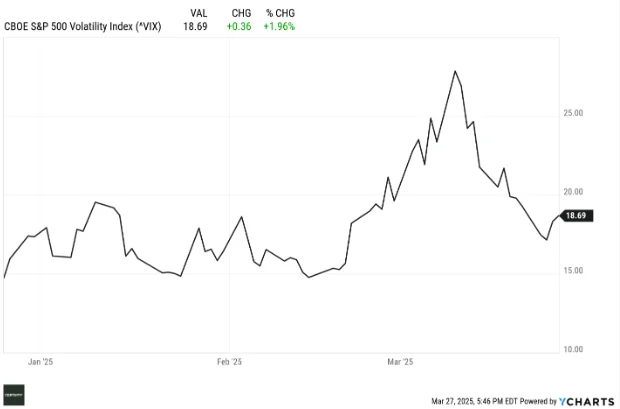

1. Market Volatility

As measured by the “VIX,” we see a rapid spike in volatility from its former quiescent levels.

Tariffs and geo-political uncertainty, combined with the release of the DeepSeek AI news -which caused great concern over the future of the US mega-cap tech stocks that have dominated the artificial intelligence (AI) narrative for the past two years – rocked the market earlier this year.

Volatility has dropped again more recently, but we fully expect to see an increased volatility regime for at least the next several months, until we have greater clarity on tariffs, regulations, and taxes.

Source: Ycharts, 3-month data through March 26, 2025. You cannot invest in an index and past performance is no guarantee of future results.

2. Consumer Sentiment

It is important to remember that personal consumption represents the majority of economic activity in the US. So, if the US consumer is feeling nervous or anxious and begins to pull back on consumption, it will have a negative effect on GDP growth.

Likewise, if business owners or CEOs lose confidence, they are likely to pull back on hiring and capital expenditure programs, potentially curtailing future economic growth.

We see this trend in a variety of industry surveys.

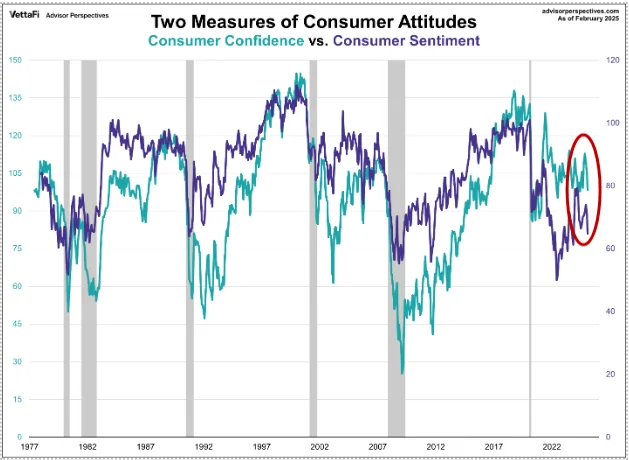

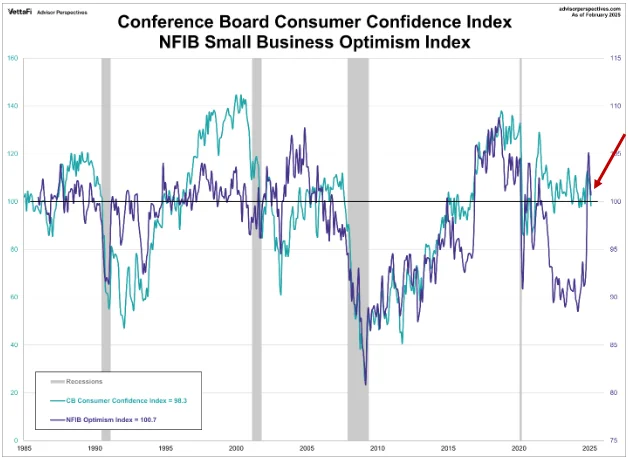

The Conference Board Consumer Confidence Index (CCI) is a monthly survey of roughly 300 households, questioning them on their “confidence” in a variety of future market conditions. The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of roughly 600 households, questioning them about personal finances, business conditions, and buying conditions.

Recent survey results for both show a bearish (or at least cautionary) trend.

Source: CCI, MCSI, and VettaFi Advisor Perspectives, as of February 2025.

The National Federation of Independent Business Owners (NFIB) is an advocacy group supporting small business owners in the US – which make up the majority of both economic activity and employment in the US.

Similar to the two consumer surveys, the most recent NFIB Small Business Owner Optimism Index shows a recent decline following a sharp spike upward following the November presidential election last year. We believe the downturn is caused by heightened uncertainty regarding the longer-term effects of Trump’s tariff policies.

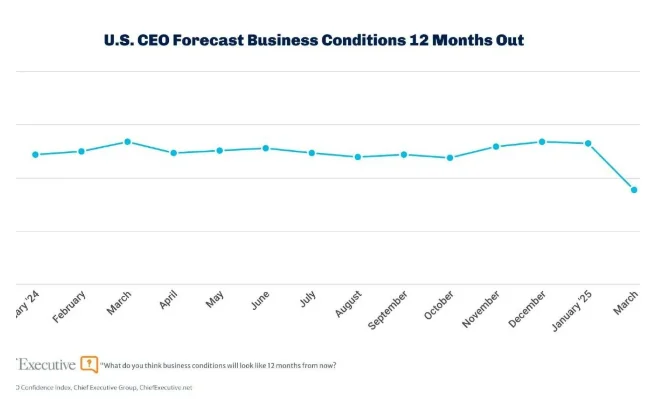

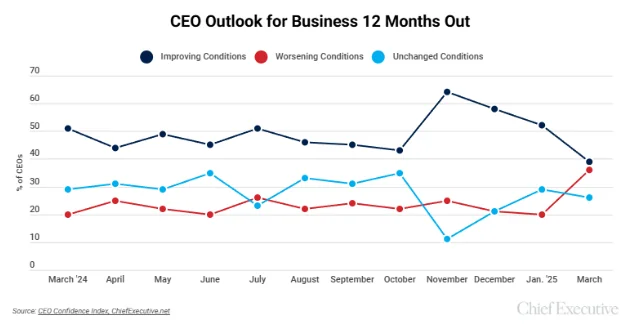

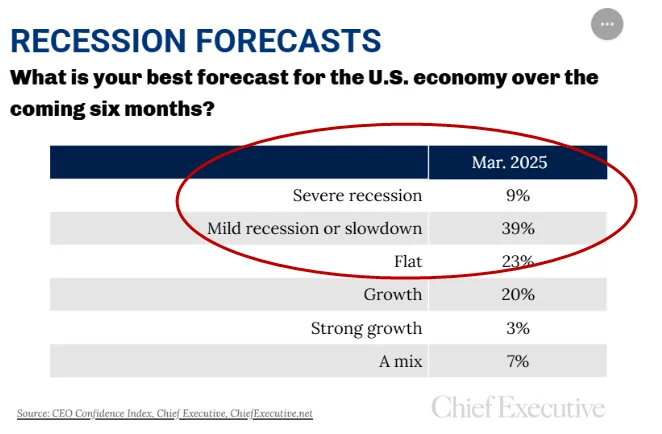

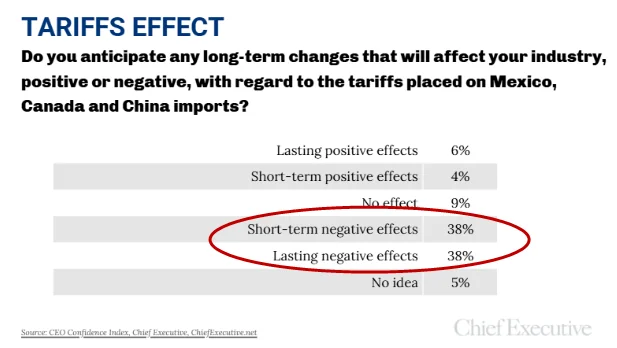

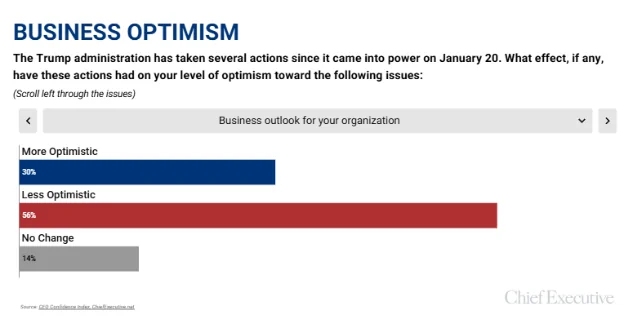

What about the CEOs of larger companies? They, too, are showing signs of losing confidence in the future direction of the US economy. Consider the following six charts, all generated from a survey by the Chief Executive Group in its CEO Confidence Index.

3. Investor Sentiment

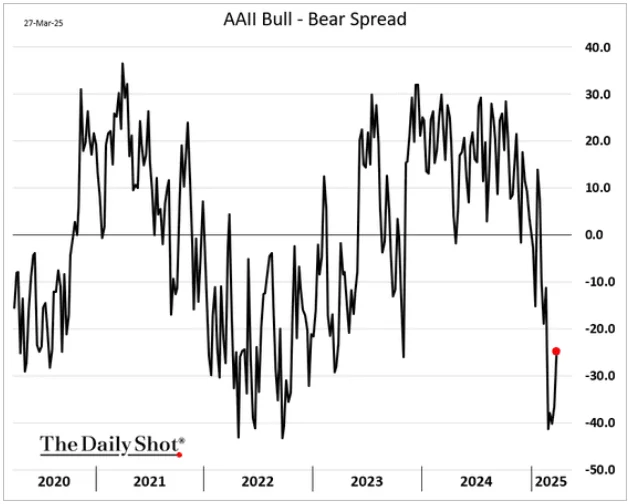

Let’s begin by looking at the American Association of Individual Investors (AAII), which publishes the “AAII Bull-Bear Spread,” the results of a weekly survey of the optimism or pessimism of individual investors regarding the direction of the stock market.

We see that sentiment moved negatively over the past two months as uncertainty has mounted. (A (a negative number represents a bearish outlook).

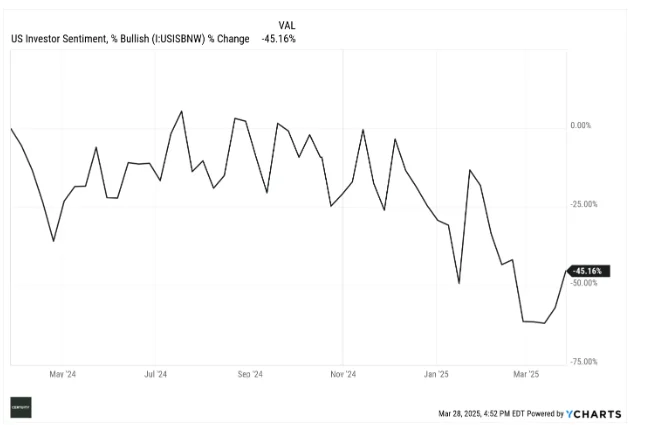

Another variation of the AAII survey is the “% Bullish” Investor Sentiment index. Here again we see a decidedly bearish move on the part of investors.

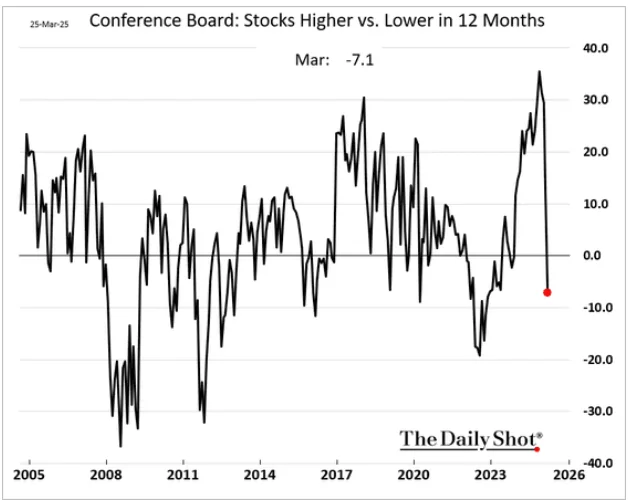

The US Conference Board sentiment metric shows a steep decline in investor expectations for stock performance over the next twelve months.

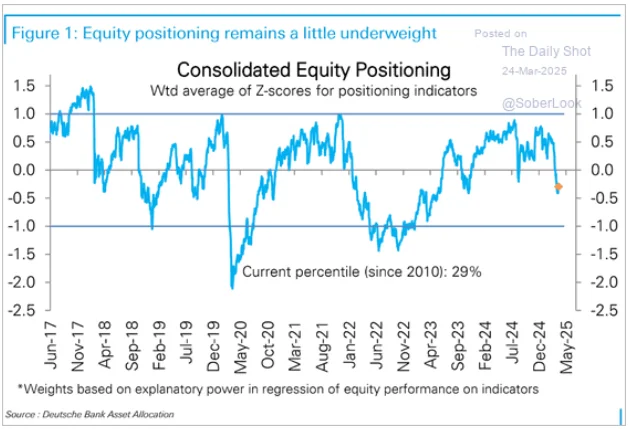

Finally, we see from Deutsche Bank that consolidated equity positioning by investors shows a marked decline in both large and small cap stocks.

4. Institutional Investor Sentiment

Theoretically, institutional investors are more “savvy” than retail investors, so what they

think is a relevant input.

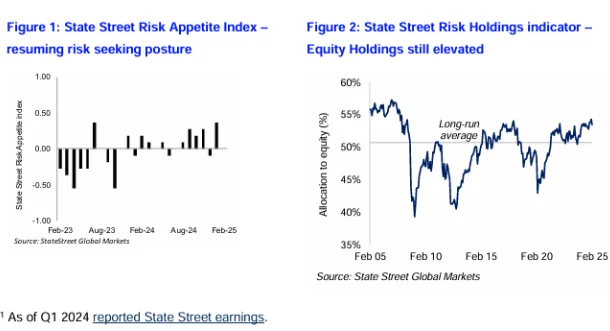

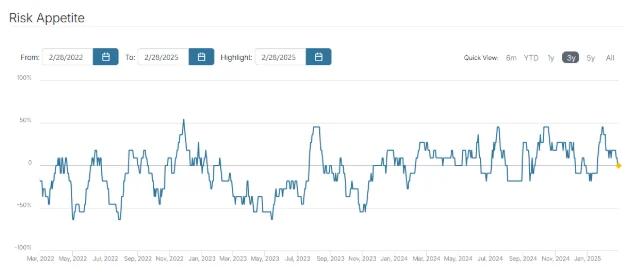

State Street Global Markets publishes a monthly “Risk Appetite Indicator” which tracks institutional investor fund flows — that is, not how they “feel” about the market but how they are actually positioning their portfolios.

We see a different perspective here than we do for retail investors. While remaining cautious, it appears that institutional investors are slowly returning to a more “risk on” positioning – perhaps believing that current uncertainty and volatility are “transitory” in nature and therefore they are “buying the dip.”

5. Equity Sentiment

Goldman Sachs regularly publishesd an “Equity Sentiment Indicator” illustrating how investors are positioning their portfolios. A “stretched” positioning indicates that investors are allocating more to equities than historical averages, while a “light” positioning indicates a more cautious allocation.

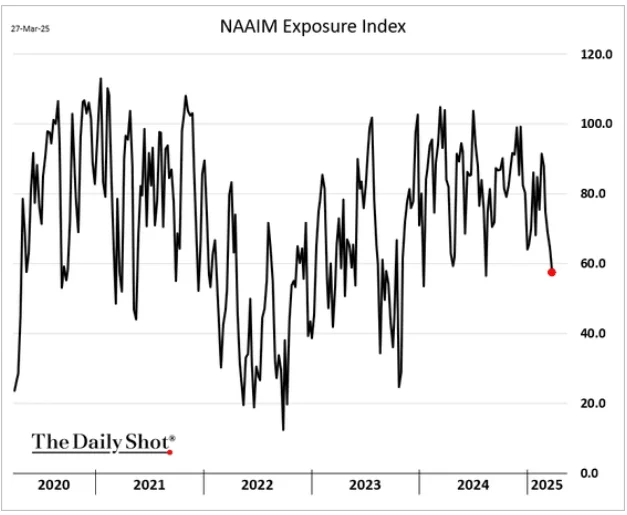

Another sentiment indicator is the National Association of Active Investment Managers (NAIIM) “Exposure Index,” which is a measure of risk adjustments active managers have made to their client accounts over the previous two weeks.

As with some of the other indicators, we see a decided move toward a more “risk off” positioning within actively managed accounts.

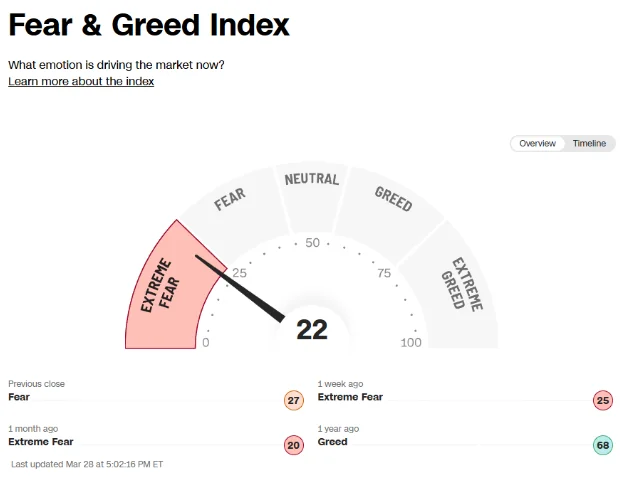

Still another sentiment indicator is the CNN Business “Fear and Greed” index, which indicates that investors have moved into an “extreme fear position, which perhaps counterintuitively may suggest an opportune time to buy. As Warren Buffett is credited with saying, “Be fearful when others are greedy and greedy when others are fearful”.

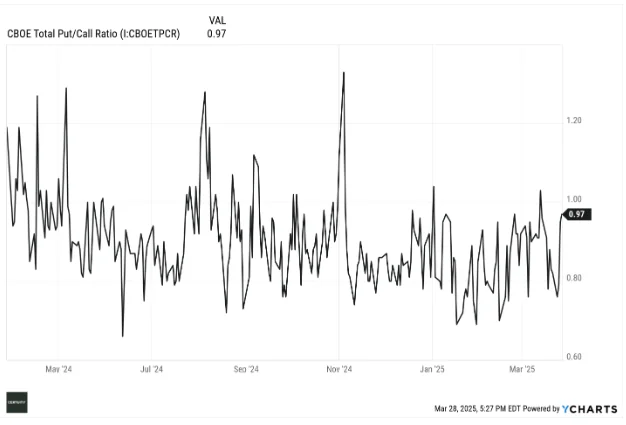

6. Put / Call Ratio

As a final measure of market sentiment, we look at the Chicago Board of Exchange (CBOE) “Put / Call Ratio,” which measures how options investors are behaving and trading.

A high ratio (>1) means more put options (the right to sell stocks) are being purchased than call options (the right to buy stocks), suggesting a bearish investor outlook.

Conversely, a low ratio (<1) implies more call options are being purchased than put options — suggesting a bullish outlook.

As you might expect, the current indication is that investors are evolving toward a more bearish outlook.

Summary and Interpretation

What these various market sentiment indicators suggest is that we currently are in a period of heightened uncertainty and anxiety. Since economic and high-level market metrics are not especially negative, we can potentially attribute this anxiety to uncertainty over the Administration’s stated regulatory, tax, and – especially – tariff policies.

The bad news is that this uncertainty is likely to last for several more months and, with it, continued volatility in the market.

The good news is that we should achieve greater clarity over time as to both the implementation and corresponding impact of those policies.

As strategic investors, we recognize it can be difficult to simply stay patient and not over-react to short-term market gyrations. But we believe that is the correct approach.

Though somewhat tongue-in-cheek, when clients call asking what they should do, we suggest they turn off their computers or TV and take their dog for a walk.

Our investment philosophy is to build “all weather” portfolios that deliver consistent performance regardless of short-term “noise” and uncertainty in the marketplace. We will, of course, recommend changes if we see a longer-term market change affecting potential returns over a reasonable time horizon.

In the meantime, we will communicate as much as possible with our clients to keep them informed, but we will also continue to recommend patience, discipline, and a focus on a longer-term time horizon.

As they sometimes say in the military, “stay frosty.”

As always, we welcome all feedback and questions.